Welcome to the non-UK founder’s guide to UK personal tax matters. This guide is designed for global business owners, founders, and digital nomad entrepreneurs who may have personal income tax liabilities in the UK. If you have a business in the UK, have tax residency status, receive dividends from a UK company, or just want to explore what personal tax obligations may arise for global founders doing business or receiving income connected to the UK, this guide is for you.

Individuals with global business operations will often have to juggle the regulations of multiple jurisdictions simultaneously. On top of figuring out the laws, licenses, authorizations, banking and tax obligations for their companies, many individuals have personal tax liabilities, sometimes in more than one country.

📚 Learn more about choosing a country of residence as a digital nomad entrepreneur

In this guide, we will focus on some of the most important UK tax and accounting obligations that apply to foreign individuals with personal income liabilities in the UK.

📚 Read more about the tax implications for non-UK founders when setting up a UK company

Part 1: Intro to personal tax obligations in the UK/around the globe

When most people think about personal tax obligations, they think about taxes they have to pay in their native country; often where they were born or are now a permanent resident, and are employed or have some other form of income.

For global founders and digital nomad entrepreneurs, personal tax obligations can be more complex, as they may have multiple sources of income from multiple different countries, and additionally may also be a tax resident in more than one country.

For example, a tax resident of the UK may be taxed on their worldwide income (i.e., derived from both UK and non-UK sources). In comparison, an individual who is not a UK resident will only be taxed on UK-sourced income.

Ultimately, individuals with global income streams need to assess whether they are considered to be tax residents under the local tax regulations. The first step for an individual who may have UK tax obligations is to assess if they are a UK tax resident.

What is the UK personal tax residency assessment / three-tier test?

In the UK, to find out if you’re considered a tax resident, you can go through the 3-tier statutory residency test. This test helps determine an individuals’ tax residency status for a specific tax year. You might hear it being referred to as the UK's personal tax residency assessment, although its official name is the Statutory Residence Test (SRT).

The three tiers are:

1. Automatic Overseas Test

This test determines if the individual has been overseas for certain periods of time and therefore considered as a non-UK tax resident for certain tax years. There are thresholds regarding the number of days that a person spends in the UK, and these vary depending on the person’s residency status prior to the tax year. For example, a previous UK resident must have been in the UK for fewer than 16 days, whereas a non-UK resident must have spent fewer than 46 days in the UK.

2. Automatic UK Test

The most popular (and commonly known) rule for the Automatic UK Test is that individuals who have spent 183 days or more in the UK during the tax year in question are automatically considered a UK tax resident for that year. There are other rules within this test, so it's best not to treat the 183 day rule at face value.

3. Sufficient Ties Test

For those individuals that fall between the overseas tier and the automatic UK tier, the status of their tax residency is decided using the sufficient ties test. Factors such as the number of days spent in the UK and types of relationships that the individual has with the UK are used to determine if the individual is considered a tax resident.

Figuring out which jurisdictions view you as a resident with tax obligations is critical for managing your tax affairs.

👉 Figure out your UK tax residency status

Tax obligations in the UK

Her Majesty’s Revenue and Customs (HMRC) is the body responsible for collecting taxes.

In the UK, tax obligations include things like:

- Filing information about your taxes (for self-employed individuals in the UK, they must file a self-assessment tax return)

- Paying taxes

- Reporting any other information in connection with your personal tax affairs

How is personal tax calculated under the UK’s tax system?

Personal income tax is calculated using a graduated or tiered system. As an individual’s income increases, they will be subjected to higher rates of tax.

Before we dive into the thresholds, it's important to note that UK tax residents can choose a 'basis' for taxation in their annual return. The standard tax treatment involves a UK tax resident having all of their worldwide income taxed and entitling them to some tax reliefs (such as the personal tax allowance described below). Alternatively, individuals can be taxed on a remittance basis*. This is available to individuals who are resident in the UK but not domicile. A person is viewed as a domicile if they are born in the UK and resident for the previous tax year or have been resident in the UK for 15 of 20 previous tax years. Individuals taxed on remittance basis will have all of their UK-sourced income taxed, however only their worldwide income that has been imported into the UK will be subject to taxation.

*As we were writing this article, the UK government announced plans to abolish the current tax treatment for UK resident non-domiciled individuals (non-doms) from 6 April 2025, after which new Foreign Income and Gains (FIG) tax rules will replace the current remittance basis treatment. Any individuals affected should seek professional guidance to understand the full implications of these changes.

Total income is calculated by considering income from all taxable sources. Deductions and allowances are available, and once applied, tax is calculated. In the UK, the main tax-free allowance is called a personal allowance and was set at £12,570 for the 2023/24 tax year. Any income over this allowance threshold is then taxed in different bands.

For example, these are the tax bands set out for the tax year of 2023/2024:

- Personal allowance (0%): Applies to income up to £12,570

- Starter Rate (19%): Applies to income between £12,571 and £14,732

- Basic Rate (20%): Applies to income between £14,733 and £50,270

- Higher Rate (40%): Applies to income between £50,271 and £125,139

- Additional Rate (45%): Applies to income over £125,140

Remember, these figures can change so always check the UK government’s website for the latest information.

What are the consequences of not paying tax in the UK?

The UK tax department has many methods of recovering unpaid tax, including debt collection, direct debt recovery (taking money directly out of a bank account), and debt recovery through increased tax rates.

Late or incorrect payment of taxes can incur penalties in the form of interest, fines, and legal proceedings, depending on the severity of the matter.

Part 2: Congratulations! You are a tax resident in the UK. Here’s what happens next.

So, you’ve discovered that you have tax residency status in the UK and need to file and pay your taxes. The first port of call is to connect with an accountant or accountancy firm. Accountancy services are a huge (and necessary) help, and can support you with completing tax filings accurately and on time, and in paying the correct amounts when they are due.

In addition to this, accountants can help you scope and plan for your taxes. By doing this as soon as you become a UK tax resident, you can understand exactly what forms, deadlines, tax fees, and other legal obligations you must address.

👉 Scope your UK tax filing and payment deadlines

How to obtain a personal tax number

Once you’ve scoped your tax obligations, you’ll need to register with the UK tax system. In the UK, individuals with personal tax obligations must start by obtaining a personal tax number called a Unique Taxpayer Reference (UTR). This is a 10-digit unique number that HMRC uses to identify individuals and their Self Assessment submissions.

Sometimes the UK tax system uses another number called a National Insurance Number (NINO) to identify tax activities. This is separate from your UTR, however the UTR is crucial for doing any personal tax reporting in the UK.

What is Form SA100?

The main tax return form used by individuals declaring Self Assessment in the UK is Form SA100, which is used to report various types of income and claim tax reliefs.

There are lots of other supplementary forms for specific circumstances:

- employees and company directors - SA102

- self-employment - SA103S or SA103F

- business partnerships - SA104S or SA104F

- UK property income - SA105

- foreign income or gains - SA106

- capital gains - SA108

- non-UK residents or dual residents - SA109

Don’t worry about all these forms, a good accountant will ensure that your SA100 is submitted with the correct supplementary pages.

When do I need to submit a UK Self Assessment tax return?

UK Self Assessment tax returns are not just reserved for individuals who are self-employed. Anyone who has multiple sources of income over a certain threshold, or who earns certain types of income such as investments, shares, dividends, and savings will need to complete a Self Assessment.

For Self Assessment taxes, the tax year begins on April 6 and ends the following year on April 5. After a tax year ends, anyone who has to file a Self Assessment tax return (and pay any taxes) can do so from April 6 onwards. The deadline is January 31, by which tax returns must be filed and paid. Missing this deadline can result in fines for which you, as an individual, are personally liable.

👉 Submit your self-assessment tax return on time

What is Form SA800?

Form SA800 is a tax return form used to declare partnership income and expenses. In the UK there are three types of partnerships:

- General partnerships

- Limited partnerships

- Limited Liability Partnerships (LLP)

A Limited Liability Partnership (LLP) is unique in that it is considered a legal entity with a separate legal personality, yet at the same time it is "transparent" for tax purposes. This transparency means that the LLP's profits are considered to be the profits of each partner in proportion to their stake in the partnership. This also changes the way that company profits are both reported and taxed.

An LLP must file an SA800 (the partnership tax return), while the amount of tax payable is determined in the self-assessment returns of each partner in proportion to their stake in the LLP.

👉 Get help submitting your partnership tax return (Form SA800)

Part 3: Exploring double taxation, capital gains tax and partnership tax liabilities in the UK for non-residents

In the previous sections we've described the general concepts and tasks connected with personal UK tax obligations. Now, let’s take a look at common scenarios that specifically affect global founders who have personal tax obligations in the UK. We’ll look at double taxation, capital gains tax and partnership tax liabilities in turn.

Paying UK tax as a non-resident doing business in the UK

Remember, if a founder is not resident in the UK under the statutory residence test then it is highly likely that they will not have to pay any UK tax on their foreign income. However, if the founder receives any income from UK sources, tax liabilities may arise.

These sources of income include things like:

- Earnings from work carried out in the UK

- Income from savings interest

- Income from UK pensions

- Dividends on shares held in UK companies

- Income from letting property in the UK

- Profits from carrying out a business (including part of a business) in the UK

Not all income sources are black and white, and so there may be instances where you need to get specialist advice to determine if your income is subject to UK taxation. For example, if you have a business that you operate remotely, but you have customers in the UK you may need to pay taxes, or if you do some work in the UK as a non-resident individual, you may need to contribute to the UK’s National Insurance scheme.

Equally, there are various allowances that you may be eligible for as a non-UK resident who is either:

- a UK national

- an EEA national

- eligible for relief under a double taxation agreement or treaty

Allowances include:

- dividend allowance

- property allowance

- personal savings allowance and starting rate for savings

- trading or miscellaneous income allowance

It’s always best to get specialist tax advice to determine which tax liabilities and tax reliefs or allowances might apply to you.

👉 Get help assessing your UK tax liabilities and tax allowance eligibility

What is double taxation and when might it apply to me?

One issue that many global founders need to handle is double taxation. This is where income may be taxed twice, in two different countries.

For example, let’s say you are a shareholder (and a non-UK tax resident) of a company registered in the UK. At a general meeting, you decide to distribute dividends to yourself based on the company's financial results of the previous year. You receive dividends from your company’s operations, but because your income comes from a UK source, you have to declare this income to UK tax authorities.

Ultimately, the risk here is that your dividends may be taxed in the UK, and again in another jurisdiction where you also have personal tax obligations (such as in Estonia, USA, etc.).

How can I eliminate double taxation in the UK?

If this situation arises in your case, all is not lost. It’s worth investigating if you can benefit from any schemes that help eliminate double taxation. Many countries have double taxation agreements (DTAs) or double taxation treaties (DTTs) in place. Each treaty determines which country has the right to levy taxes on different types of income and in different circumstances.

The good news is, the UK has lots of treaties with different countries and so individuals may qualify for full or partial exemption from income tax if they are dual tax residents in the UK and another country that has a DTT with the UK. In cases where a country does not have a double taxation treaty with the UK, individuals may still be able to obtain a unilateral tax relief for foreign taxes paid.

👉 Find out if you can eliminate double taxation

What is UK capital gains tax and when might it apply to non-residents?

Capital gains tax (CGT) is a tax charged on the profit or gain made when selling, giving away, exchanging, or disposing of an asset that has increased in value. In the UK, CGT rates vary depending on factors such as an individual’s income tax band and the type of asset sold. There are also some allowances and reductions that may reduce CGT amounts, and certain assets may be exempt from CGT altogether, like assets that are considered gifts to spouses or charities.

In the UK, generally, capital gains tax only applies to UK residents. There are a few exceptions in which capital gains tax applies to non-residents who sell certain types of UK assets. General guidance is available for non-residents who are domiciled in the UK. Remember, domicile is not the same as nationality, citizenship or residence; you are domiciled in a country that is considered your permanent, long-term home, or in the country where you consider your “roots” are. For individuals who are not domiciled in the UK, different guidance applies so it is best to consult with a professional about CGT liabilities.

👉 Get an analysis of your capital gains tax liabilities

What capital gains taxes might apply to gains on UK property disposal?

UK domiciled non-residents will have to pay capital gains taxes when there is a sale or “disposal” of specific assets like UK land and UK property. The amount of CGT or NRCGT due will vary depending on when a property was purchased, when it was disposed of, and whether it is classified as residential, non-residential or partly residential. Therefore, it is very important to seek professional advice as to what capital gains tax liabilities may apply, the deadline for notifying HMRC regarding CGT matters, and the deadline for making payments of any tax owed.

👉 Find out if gains on your UK land and property disposal triggers CGT or NRCGT liabilities

Do I have to pay UK partnership tax if I’m a non-resident?

As discussed earlier, Form SA800 is used to file tax returns on profits and expenses for partnerships. If you are not a UK resident and do not reside in the UK while you and your UK resident partner are members of an LLP, then all LLP profits are declared in the SA800 form. At the same time, you and your partner pay taxes on the LLP's profits separately in your personal tax returns. Your UK resident partner files a return in the UK and determines the tax payable in proportion to their stake in the partnership. For example, if their contribution (share) in the LLP is 30%, and the annual profit of the partnership is 100,000 GBP, then in their personal declaration they will indicate 30,000 GBP as their personal income.

Now, as you are not a UK resident, you will declare your income from the partnership, which in our example is 70,000 GBP (according to your 70% stake in the LLP), in your tax return in the jurisdiction where you are a tax resident.

The question then arises: does the UK also have the right to tax your income received by the LLP? The answer depends on several factors, including what income the LLP received and specifically, whether any of the income originates from the UK. If the answer is yes, you will probably have tax obligations in the UK as well, which will need to be fulfilled by filing a UK tax return and paying your taxes on time.

👉 Get help submitting your partnership tax return (Form SA800)

Manage all your personal and company tax matters in one place

Managing taxes across multiple jurisdictions, and in countries where you may not be familiar with tax systems and practices, can be quite challenging. Legal Nodes helps global entrepreneurs to figure out both their personal and their corporation tax liabilities and ensure that deadlines for filing and payments are always met.

We work with a global network of tax and accounting experts, including specialists in the UK. We support individuals with various tax residencies, including digital nomad entrepreneurs, and those with business operations and investments across multiple countries. Through Legal Nodes subscriptions and add-ons, we empower business owners to comprehend their global tax obligations both on a personal and company level.

Whether you require ongoing assistance with tax reporting and accounting duties in the UK or just need answers to specific questions, Legal Nodes is here to support you. Kickstart your journey towards efficient tax management and financial compliance: speak to us to get started.

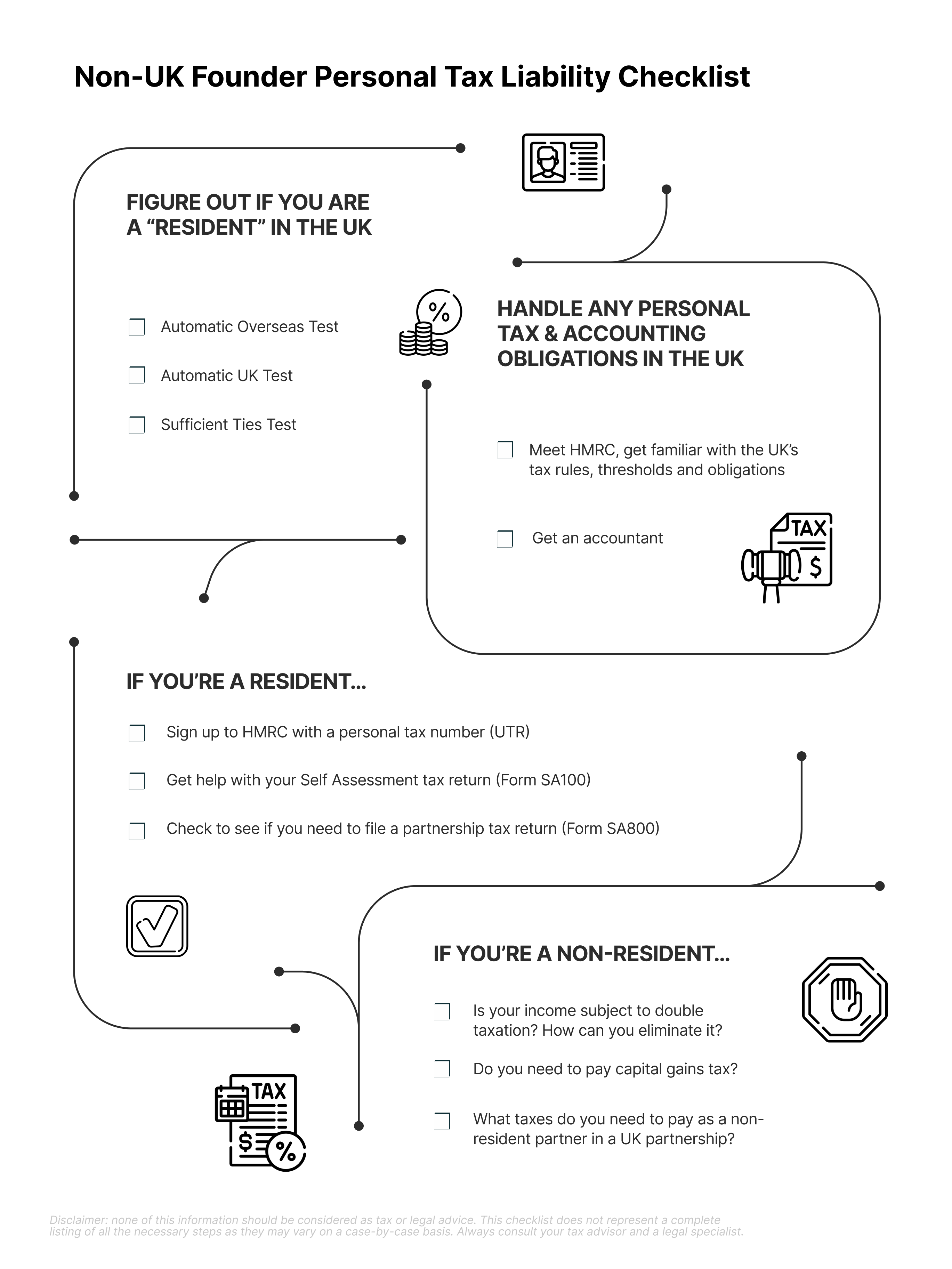

Non-UK Founder Personal Tax Liability Checklist

- Figure out if you are a “resident” in the UK:

- Automatic Overseas Test

- Automatic UK Test

- Sufficient Ties Test

- Get ready to handle any personal tax and accounting obligations in the UK:

- Meet HMRC, get familiar with the UK’s tax rules, thresholds and obligations

- Get an accountant

- If you’re a resident…

- Sign up to HMRC with a personal tax number (UTR)

- Get help with your Self Assessment tax return (Form SA100)

- Check to see if you need to file a partnership tax return (Form SA800)

- What else do you need to think about?

- Is your income subject to double taxation? How can you eliminate it?

- Do you need to pay capital gains tax?

- What taxes do you need to pay as a non-resident partner in a UK partnership?