The founders of Web2 companies are used to the fact that their fundraising usually starts with Pre-Seed/Seed rounds and then continues with rounds A, B, C, D, and so on - until an exit or IPO. But the founders of Web3 companies structure their rounds differently, and the liquidity event of their companies is not always an exit or an IPO.

This article will discuss the different investment rounds that are usually used by Web3 companies, and will explore the expectations of founders and investors during each round. Finally, this article will evaluate how each round is typically structured from a legal perspective.

🏴 If you're planning a token distribution, you'll need understand the legal implications of your plans, and put a comprehensive legal strategy in place. Not sure where to begin? Check out our latest playbook to get started: How to Build a Legal Strategy for a Token Project

Investment rounds of Web3 companies

Web3 founders often allocate the following fundraising rounds:

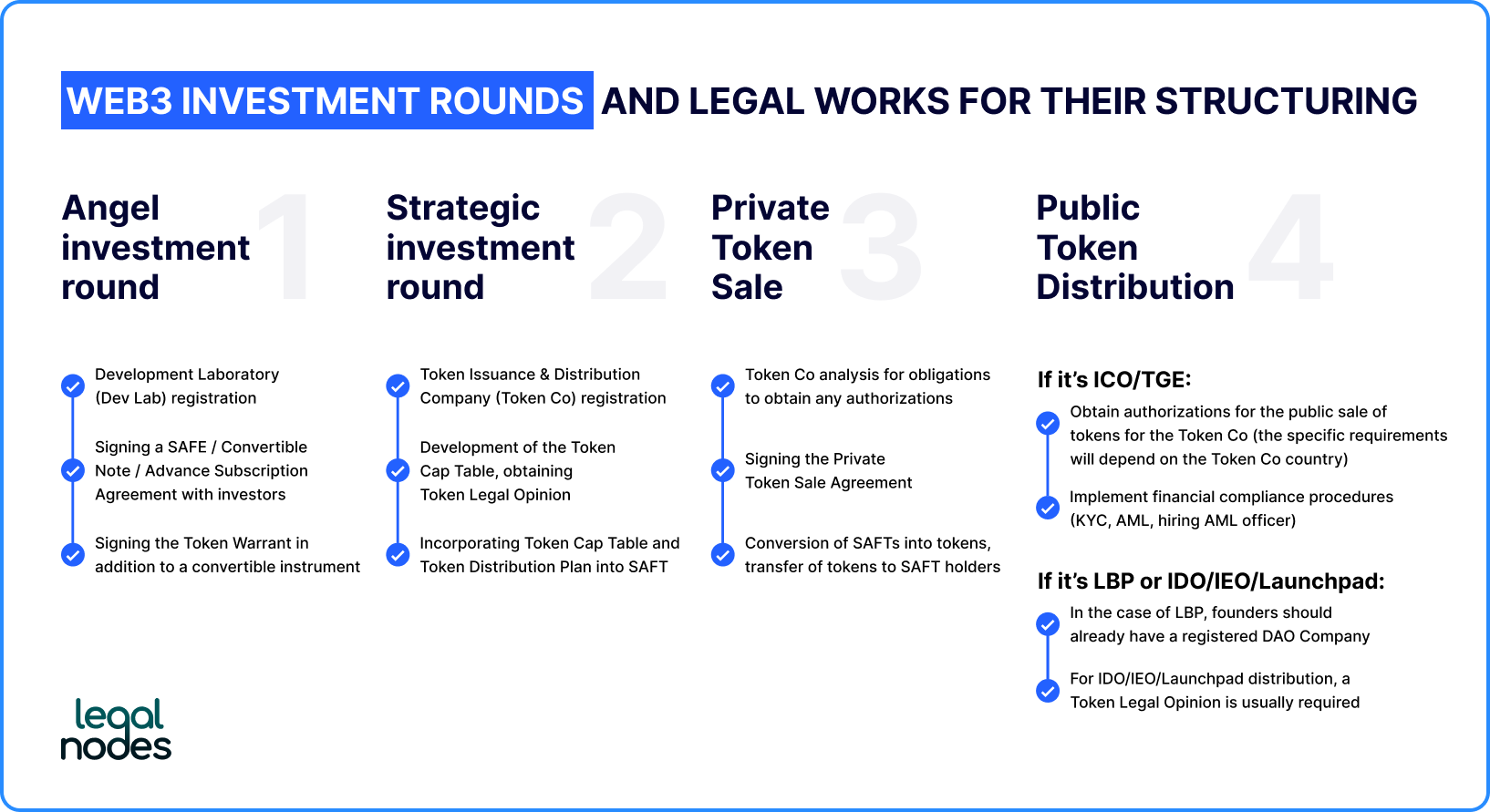

- friends & family, business angels investment; the Web2 sphere usually calls this round the "pre-seed/seed" and it is during this round that the first people are hired and begin working on the proof-of-concept;

- strategic round; during this round, founders begin to develop the tokenomics and choose a blockchain network;

- private token sale; the founders attract their first large token holders and prepare for the public launch of their token;

- public token sale; the founders publicly launch their token for the growth of their product/protocol and to start building a community of token holders.

Angel investments and their legal structuring in Web3

An angel investment round is usually the first investment round, during which Web3 founders want to attract initial funding to hire the first people in the team and start testing their idea, developing the concept, and finding a product-market fit. At this stage, Web3 founders are usually unsure whether they will issue their tokens and whether the project will eventually turn into a DAO.

In this round, the key expectations of investors are to receive a share in the company that owns the product's IP rights and the right to tokens (in case the Web3 founders decide to issue tokens in the future).

Taking into account the founders’ plans and the investors’ expectations for this investment round, the following legal works are necessary for its structuring:

- registration of a development company (Development Laboratory), the captable of which will have founders and an option pool, and all intellectual property rights will be registered to the company;

- signing a convertible instrument such as a SAFE / Convertible Note / Advance Subscription Agreement or other type of convertible instrument for equity investment with investors;

- signing the Token Side Letter addendum to the convertible instrument for equity investment, which will entitle investors to receive tokens in the future if the founders decide to issue them.

📝 FREE TEMPLATE: Check out and download the Token Side Letter template for pre-seed fundraising

Strategic investment round

After the Web3 founders have reached the proof of concept stage, meaning that they have hired a team, developed an MVP, and validated it with potential users, they move on to work on tokenomics for their product/protocol. The tokenomics is designed to achieve several goals:

- launch a native token for the implementation of an incentive model to increase the engagement of users of the product/protocol;

- increasing the product recognition and expanding the audience of its users through public token distribution;

- creating the possibility of converting the future community of token holders into a decentralized organization with its treasury and governance (a DAO).

To successfully implement these goals, the founders need to choose the blockchain on which the tokenomics will be launched and the ecosystem partners who will help with its implementation (for example, exchanges, wallets, and liquidity pools). This round is often called "strategic" since the foundations of large blockchain protocols, crypto exchanges, large DeFi, and more, often participate in it.

Strategic investment round legal structuring

Before moving on to the legal works necessary for structuring a strategic investment round, it is important to emphasize the expectations of investors and the guarantees they want to receive from the Web3 startup in this round. Expectations include receiving tokens at a discounted price, guarantees that there are no legal restrictions on the issuance and distribution of tokens, and in some cases, the right to control the process of token issuance and distribution.

Taking into account the founders’ plans and the investors’ expectations for this investment round, the following legal works are necessary for its structuring:

- registration of the Token Issuance & Distribution Company (Token Co), which will be responsible for the initial issuance and distribution of tokens;

- development of the Token Cap Table, determination of the sale price of tokens and the stages of their distribution, obtaining a Token Legal Opinion to analyze whether there may be legal restrictions on the liquidity of such a token in the future;

- displaying the details of the Token Cap Table and Token Distribution Plan in the SAFT (Simple Agreement for Future Tokens), and in some cases - signing the SAFTE with investors (if investors want to receive not only tokens in the future but also the level of control over the process of issuing and distributing tokens for ownership of Token Co shares).

📚 Read more: Choosing a Web3 Fundraising Document: a Playbook for Web3 Founders

Private Token Sale

If, at the beginning of the previous investment round (the strategic round), Web3 founders only had a Token Cap Table and a general plan for Initial Token Distribution, then as of the beginning of the Private Token Sale, most investors will expect the following from Web3 founders:

- tokenomics that is integrated into the product/protocol of Web3 founders and which has reached market-fit in the process of private testing;

- a well-thought-out plan for Public Token Distribution that should help founders to create a powerful community of token holders and investors to receive investment income when the token becomes liquid.

This, in turn, defines the key objectives of the founders in the Private Token Sale round, namely to attract investments that will help:

- finance the Public Token Distribution; as well as

- create a large community of token holders to promote the use of the Web3 product/protocol.

📚 Read more: Models of token distribution and how to legally structure them

Legal structuring of Private Token Sale round

An important aspect of this round is that–at this moment–the tokens are already pre-minted, and the first sale of these tokens involves not only their private sale transfer to investors (with a token lockup) but also the conversion of investors' SAFTs from the previous round.

Thus, the following legal works are required for the legal structuring of the Private Token Sale:

- analysis of the Token Co for whether it has obligations to obtain special authorizations/permits to start selling tokens (authorizations may include both VASP and specific securities-related authorizations such as Reg. D / Reg. S in the USA);

- signing of the Private Token Sale Agreement, transfer of pre-minted tokens to investors with a lockup condition (usually, the first 12-36 months after the Private Token Sale, the tokens are blocked/illiquid to avoid the risks of price manipulation);

- conversion of SAFTs into tokens, transfer of tokens to SAFT holders under the terms of SAFTs.

Public Token Distribution

The main purpose of the investments involved in the Private Token Sale stage is to organize a successful Public Token Distribution campaign, namely: to prepare a powerful marketing campaign to start building a community of future token holders in advance, as well as to attract the necessary partners (exchanges, launchpads), which already have their audiences of users interested in the new token. An important aspect of this investment round is the choice of a method for public token distribution, as the legal requirements for its implementation will depend on this.

To date, these methods of public token distribution can be conventionally distinguished as the following:

- ICO/TGE which stands for Initial Coin Offering and Token Generation Event. An ICO/TGE is a method of public token distribution that involves the public sale of tokens from the company's website with the receipt of payments for these tokens in the Token Co treasury;

- LBP which stands for Liquidity Bootstrapping Pool. An LBP is a method of public token distribution that provides for the possibility of receiving tokens through the deployment of an equivalent amount of other virtual assets in the DAO liquidity pool, from which these assets will be reinvested to improve tokenomics);

- IDO/IEO/Launchpad which stands for Initial DEX Offering and Initial Exchange Offering is a public token distribution method that involves a third party, an intermediary for the public paid distribution of tokens.

Legal structuring of Initial Coin Offering/Token Generation Event

The legal requirements for conducting this kind of public token distribution campaign will depend on which type of public token distribution was chosen and in which jurisdiction the Token Co is registered. Another factor that will affect the legal structure of the public distribution of tokens is the recipient of the proceeds from the public sale of tokens.

Based on these criteria, in the case of legal structuring for ICO/TGE token distributions, the distribution itself will be a centralized sale of tokens with subsequent receipt of the proceeds from this sale to the Token Co. This, in turn, requires the Token Co to obtain the necessary authorizations/licenses for the public sale of tokens (VASP, securities/collective investment schemes authorizations), as well as to implement the necessary financial compliance procedures, for example, KYC and AML procedures for the sale of tokens, and hiring an AML officer to monitor these procedures.

📚 Read more: Investor due diligence checklist for Web3 founders

LBP & IDO/IEO/Launchpads legal structuring

In the case of token distributions through the Liquidity Bootstrapping Pool, the legal structuring requirements are a little different. When launching the campaign, the founders must have already registered a DAO company. This company will act as a governance wrapper for DAO members who will manage the liquidity pool formed due to the public distribution of tokens through the LBP.

In the case of token distributions via an Initial DEX/Exchange Offering or via Launchpad, the exchange/launchpad provider will act as an intermediary between the token-issuing company and the community of token buyers. This means that, in most cases, the requirements for the verification of token buyers and the verification of the source of their funds will fall on the platforms to meet and resolve. At the same time, these platforms will, in most cases, require a Token Legal Opinion from projects to avoid any risks associated with distributing non-compliant tokens.

Future rounds of token distribution

Conducting a public token distribution campaign allows Web3 founders to create a community of tokenholders, which can later be structured into a decentralized organization (DAO). In this regard, in most cases, such a primary public token distribution campaign becomes the last round of fundraising, which is conducted and structured centrally (namely, by the project's founders).

After the completion of the initial public token distribution and the launch of the DAO, the decision regarding the future additional issuance of tokens and additional liquidity attraction in the DAO Treasury is being made by the members of the DAO through on-chain voting in line with the DAO Constitution. The founders of the project become the members of the DAO and, in many cases, can occupy a representative/executive role in the DAO, depending on the DAO management bodies provided for in the DAO Constitution.

📚 Read more: Launching a DAO: the 3 stages and legal works for DAO projects

How to prepare your Web3 project for the investment round

Depending on which investment stage your project is at right now, the type of legal support you may require will vary. At Legal Nodes, we help Web3 founders get a clearer idea of their next steps and prepare for upcoming investment rounds. Start by requesting a demo call to find out how we could help you.

Disclaimer: the information in this guide is provided for informational purposes only. You should not construe any such information as legal, tax, investment, trading, financial, or other advice. Mentioning any of the assets in this article is not an endorsement to purchase them.

Prepare for Web3 investor due diligence with help from Legal Nodes

Nestor is a Co-founder & Head of Web3 Legal at Legal Nodes. Having over seven years of legal consulting experience, Nestor loves working with innovative startups and Web3 projects, helping them navigate the regulations and scale on global markets.